Thursday, September 25, 2008

Mr. Mortgage asserts that the funding is insufficient to address the bad debt that the collapse of the housing market continues to generate:

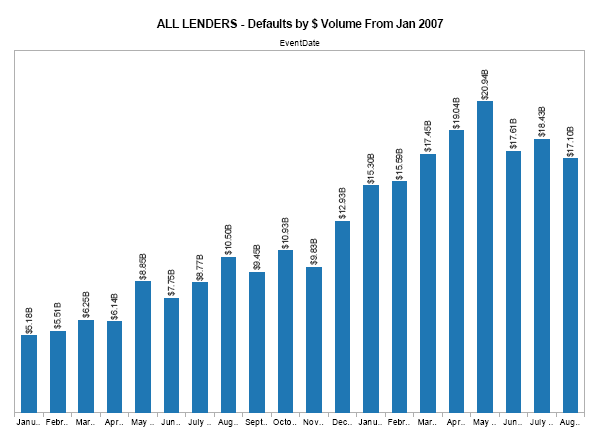

Meanwhile, after listening to the testimony of Federal Reserve Chairman Barnanke yesterday, CR is equally dubious:$700bb will not go too far. Below is a custom chart of loan defaults from all lenders for the State of CA from Jan 2007 to present. CA represents about 40% of the total dollar volume in the nation.

As you can see defaults have leveled off in the summer at record high levels, which is not surprising due to seasonality, hope and the transition out of Subprime into other grades of paper. What you see below is primarily only the ‘Subprime Implosion’. However, the numbers are still near $20bb per month. This means the numbers are closer to $40-$50bb on a national level.

As we exit the Summer season and housing demand falls (surprisingly fell sharply in Aug - See Aug CA Home Sales Report), defaults should pick back up again as values fall. Early signs indicate a severe fall going into Winter. Subprime defaults will continue for much longer given the number of new defaults we are seeing and the 50% recidivism rate amongst modified subprime loans. This is mostly due to negative equity and borrowers simply finding it cheaper to rent.

But the new waive of housing defaults will come from the Alt-A (includes Pay Options), Jumbo Prime and the Second Mortgage universes. This is also due to values being down so much in the bubble states and the negative equity effect. CA prices are off 30-60% depending in the region in the past 16-months.

{kind=link}

Of course, the conventional wisdom is that the injection of funds into the global financial institutions holding these nearly worthless securities will result in reinvigorated lending activity. Mr. Mortgage is pessimistic:And a final point, many people are saying the government can only lose a portion of the $700 billion because there will be offsetting assets. This is true in the Fannie and Freddie conservatorship (the mortgage assets mostly offset the debt of Fannie and Freddie), but it is not true here. Although Paulson and Bernanke are talking about hold-to-maturity prices, they are also talking about both buying and selling securities. A little math will show that if you take a loss (say 30%) on each transaction, it doesn't take many transaction to lose most of the entire $700 billion.

Economist Michael Hudson expands upon Mr. Mortgage's analysis to alarming effect:Perhaps this program will grease the wheels, everyone will begin lending again and home values will soar making it so home owners can freely sell or refinance. But given the data I see daily, I am betting against that. The problem is, anything short of physical real estate being a liquid asset once again or an across the board principal balance reduction and new terms on every loan in America, and the housing crisis remain front pages indefinitely as the negative equity feedback loop continues and more borrowers are forced into loan default each month.

But are we naive to believe that the bailout is really about resolving a financial crisis that is enveloping the neoliberal world? For example, read between the lines of this excerpt from an article by William Greider, posted on The Nation website:There is a reason why the banks won’t lend: Housing and commercial real estate already are so heavily mortgaged that there is no rental value available (over and above operating expenses, current taxes and debt service) to pledge to the banks. It still costs more to buy a house than to rent it. No increase in the amount of credit, short of hyper-inflation can cure this. No lowering of interest rate, will lead banks to risk making a bad new loan – that is, a loan that probably will go bad and end up with the bank taking a loss after the borrower walks away or defaults.

Does Congress know what it is being told to do? Suppose that “taxpayers” are to squeeze money out of the “toxic” junk mortgages they buy from the investors that have bought these bad loans. The only way to do so would be for real estate prices to be raised to even higher levels. This means an even higher proportion of take-home pay by prospective homeowners.

Mr. Paulson realizes this. That’s why he’s directed Fannie Mae and Freddie Mac to inflate real estate prices all the more. At least, by the existing mortgage-holders to get paid off by existing debtors selling to the proverbial “greater fool.” The hope in Mr. Paulson’s plan is that there are enough “greater fools” with enough money to borrow from yet more foolish new mortgage lenders. Only Fannie Mae, Freddie Mac and the Federal Housing Agency are willing to make such foolish loans, and that is only because they are being directed to act in a foolish way by Mr. Paulson.

Here’s the problem with following Mr. Paulson’s orders and lending yet more: Every major real estate advisor on record has forecast a further drop of between 20 to 30 percent in property prices over the coming twelve months. This is now the standard forecast. It means that over and above the five million arrears and foreclosures that Mr. Paulson acknowledged already are on the books, yet more families are to give up the fight by this time next year. Is the $700 billion giveaway fund to try and recoup by evicting them too from their houses – to pay the “taxpayer” enough to bail out Countrywide, Washington Mutual and other predatory lenders for loans that state Attorneys General have accused of being fraudulent?

For the government to even begin to recover some of the value of the $700 billion in junk mortgages it has bought would force new homebuyers to pay even more of their income to the banks. And if they do that, they will have less income to spend on goods and services. The domestic market will shrink, and tax revenues will fall at the state, local and federal levels. The debt overhead will deflate the economy, causing shrinkage all down the line.

So here’s where the cognitive dissonance comes in: It is necessary, even inevitable, for the volume of debt to come down – not up – to restore equilibrium. The economy was well on its way to preparing the ground for this last week. As Alan Meltzer of the American Enterprise Institute (of all places!) explained on McNeill-Lehrer, Merrill Lynch was able to be sold at 22 cents on the dollar; and the economy survived Lehman Brothers and Bear Stearns being wiped out.

Such debt writes-offs are a precondition for writing down America’s mortgage debts to levels that are affordable. But Mr. Paulson’s plan is to fight against this tide. He wants the Wall Street to keep on raking in money at the expense of the economy at large.

We can summarize Greider's evaluation of socioeconomic implications of the bailout in one sentence: Paulson and Bernanke hope that the bailout will encourage financial institutions to generously make credit available again, but they want to make certain that the Federal Reserve, the Treasury and investment banking firms like Goldman Sachs and Morgan Stanley retain their dominant roles in the global economy.Wall Street put a gun to the head of the politicians and said, Give us the money--right now--or take the blame for whatever follows. The audacity of Treasury Secretary Henry Paulson's bailout proposal is reflected in what it refuses to say: no explanations of how the bailout will work, no demands on the bankers in exchange for the public's money. The Treasury's opaque, three-page summary of plan includes this chilling statement:

In other words, no lawsuits allowed by aggrieved investors or American taxpayers. No complaints later from ignorant pols who didn't know what they voted for. Take it or leave it, suckers."Section 8. Review. Decisions by the Secretary pursuant to the authority of this Act are non-reviewable and committed to agency discretion, and may not be reviewed by any court of law or any administrative agency."

Both political parties may submit to this extortion because they don't have a clue what else to do and bending over for Wall Street instruction, their usual posture, seems less risky than taking responsibility. Paulson and Bernanke evoked intimidating pressure for two reasons. The previous efforts to restore investor confidence had all failed as their slapdash interventions worsened the global panic. Besides, the Federal Reserve was running out of money. Nearly three-fifths of the Fed's $800 billion portfolio is now loaded down with junk--the mortgage securities and other rotten assets it took off Wall Street balance sheets. The imperious central bank is fast approaching its own historic disgrace--potentially as discredited as it was after the 1929 crash.

Despite its size, the gargantuan bailout is still designed for the narrow purpose of relieving the major banks and investment houses of their grief, then hoping this restores regular order to economic life. There are lots of reasons to think it may fail. The big boys are acting, as usual, in self-interested ways since the government allows them to do so. Washington's money might pull firms back from the brink--at least the leaders of the Wall Street Club--but that does not guarantee the banks will resume normal lending, much less capital investing. The financial guys may well hunker down, scavenge the wreckage for cheap profits and wait for the real economy to get well. Likewise, global investors--China, Japan and other major creditors--have been burned and may step back from pumping more capital in the wobbly house of US finance.

Secrecy and opacity are crucial to achieve Wall Street's purposes. It could allow Paulson to overpay his old pals for near-worthless assets and slyly recapitalize the damaged banks while telling public and politicians the money is to save the system. To achieve this, Wall Street needs to keep control of the process whoever is elected president (the Wall Street Journal recommends John Thain, ex-chief of the New York Stock Exchange to succeed Paulson). Not everyone will be saved, of course, but high on the list of endangered nameplates is Goldman Sachs, Paulson's old firm. The high-flying investment house looks doomed by these events. The Fed quickly agreed to convert Goldman and Morgan Stanley into banks. Think of Paulson's solution as Goldman Sachs socialism.

Hudson expands upon Greider's notion that financial guys may well hunker down, scavenge the wreckage for cheap profits and wait for the real economy to get well:

I'm not as sure about this as Hudson, but I do believe that it will move American society in this direction, making day to day life more difficult for the vast majority of Americans, while enhancing the power of the financial interests that are responsible for the crisis. As with the "war on terror" and the Iraq War, failure, and the fear that it engenders among the populace, has become an essential instrument for consolidating political and economic power.If Congress should be so destructive as to buy out $700 billion of bad loans (for starters), the sellers will do just what Russia’s kleptocrats did. They will take their money and move it abroad to a “hard” currency country. This will help collapse the dollar. Up will go gasoline costs and prices for other imports. America will be turned into a Russian-style post-Soviet economy, having endowed a new domestic kleptocracy of insiders, who use some of their gains to finance the campaigns of American Yeltsins such as McCain.

And the elites behind these policies have succeeded beyond their most exuberant expectations. After 9/11, they persuaded Congress to relinquish much of its power to exercise oversight of law enforcement by passing the Patriot Act, and more recently, the evisceration of FISA. Much of this power is now securely esconsced in the executive branch. By authorizing the invasions of Iraq and Afghanistan, and approving funding for militarized covert operations around the world, Congress has abdicated its constitutional responsibility to restrain the war powers of the presidency. Now, with the impending passage of this bailout, Congress is about to reliquish its responsibility to ensure transparent regulation of the financial markets by permitting the Treasury to secretly intervene whenever it deems necessary to purchase billions of dollars of nearly worthless mortgage backed securities.

Back in 2004, the Retort collective described the current global economic order as military neoliberalism in their seminal work, Afflicted Powers, initially published as a New Left Review article and subsequently expanded into a provocative book. It emphasized that when the US and neoliberal interests cannot impose neoliberal policies, generally defined as fiscal austerity, deregulation, privatization and the free flow of capital, through coercion, by recourse to US controlled global financial institutions like the IMF and the World Bank, they resort to force, as they have done in Iraq, and, to a much more subtle degree, in Venezuela and Bolivia. With the Treasury and the Federal Reserve already massively intervening in financial markets to the tune of hundreds of billions of dollars, with the prospect of hundreds of billions of dollars more available if the bailout is passed, the existing order might be more accurately described as militaristic crony capitalism, because the elites and financial institutions responsible for creating an economic order based upon broadly recognized neoliberal principles have openly repudiated these principles to preserve their hegemony, thus fatally impairing the ideological integrity of the project. Not even the corporate control of much of the media can conceal what has transpired.

Everyone now recognizes that the discipline of the markets is only for people weak enough to have to accept their subjugation to them. If you are economically and politically powerful enough (and, doesn't one necessarily lead to the other?), you can manipulate the processes of the state to exempt yourself from them. The profound effort to transform the capitalist societies of Europe, Asia and the Americas by persuading the populace that markets are superior to the political process in adjudicating disputes associated with the allocation of resources is dead. A post autopsy question remains: will the exposure of the fraudulent nature of this endeavor result in the revival of political processes that have been discredited? If so, there will be opportunities for progressive change. If not, if people are now disgusted with both the markets and the political process, then the road is open to authoritarism. Sadly, I fear that the latter is more probable.

To put it more starkly, the crisis is being manipulated for the purpose of accomplishing the complimentary goal of concentrating power within the dominant capital class. Greider alludes to it, but fails to understand the pulverizing scope of this aspiration, seeking refuge by limiting it to Goldman Sachs and Morgan Stanley. In a fascinating book, The Global Political Economy of Israel, political economists Jonathan Nitzan and Shimshon Bichler interpret the last 50 years of global economic history, at least as it relates to the US, Israel and the Middle East, in terms of what they describe as the capitalisaton of power. Put simply, they contend that a class of dominant capital exists, and that this class will manipulate economic events to concentrate more and more power within itself.

Accordingly, it is the accumulation of economic power that is primary, not the accumulation of wealth. You would think that the two walk hand in hand, but, as demonstrated by Nitzan and Bichler, they don't always do so. If the expansion of the economy is creating greater and greater opportunities for smaller competitors, providing them with returns that threaten the primacy of dominant capital, then it prefers an economic downturn to crush these emerging competitors less able to weather such difficult conditions. To achieve this, dominant capital will accept lower profits, and even losses and reduced size, because it is concerned about reversing a decline in its relative relationship of power. Profits will return another day.

We can only speculate as to what provoked this particular crisis. Did the housing bubble go too far and result in the creation too many small and medium sized competitors with greater returns on investment, thus necessitating the termination of a system of easy access to subsidized credit for them? Is the ensuing credit crunch being manipulated for this purpose? If so, the financial crisis is not a failure, as I have described it, but rather a deliberate policy of creative destruction ignited to eliminate competition. Others have observed that the invasion and occupations of Iraq and Afghanistan can be construed in a similar way. Certainly, if one looks at the current credit freeze, one wonders. Will the expenditures authorized by the bailout serve to benefit the interests of dominant capital over the interests of its competitors? If this is the true purpose, wouldn't it be best accomplished by underfunding the bailout, so that only a privileged few could participate? Indeed, isn't it necessary to structure the bailout so that dominant capital obtains relief, while its lesser competitors asphxiate?

Obviously, answering such questions requires an expertise and research effort beyond my capabilities, although this is clearly the gist of the recent articles by Michael Hudson posted at Counterpunch. I encourage readers to go that site and peruse the last two or three weeks or articles in order to find them, or conduct a web search for them with the terms "Michael Hudson" and "Counterpunch" and any other useful variations. His articles, as with the excerpts from the one that I have posted here today, provide some counterintuitive insights. As already discussed here, one of the most frightening aspects of the crisis is the extent to which dominant capital may have determined that it has no alternative but to instigate extreme social and economic instability to preserve its power.

Labels: American Empire, Bailout of Finance Capitalists, Credit Crunch, Housing Bubble, Neoliberalism

![]()